- Europe-Africa Initiative

- Posts

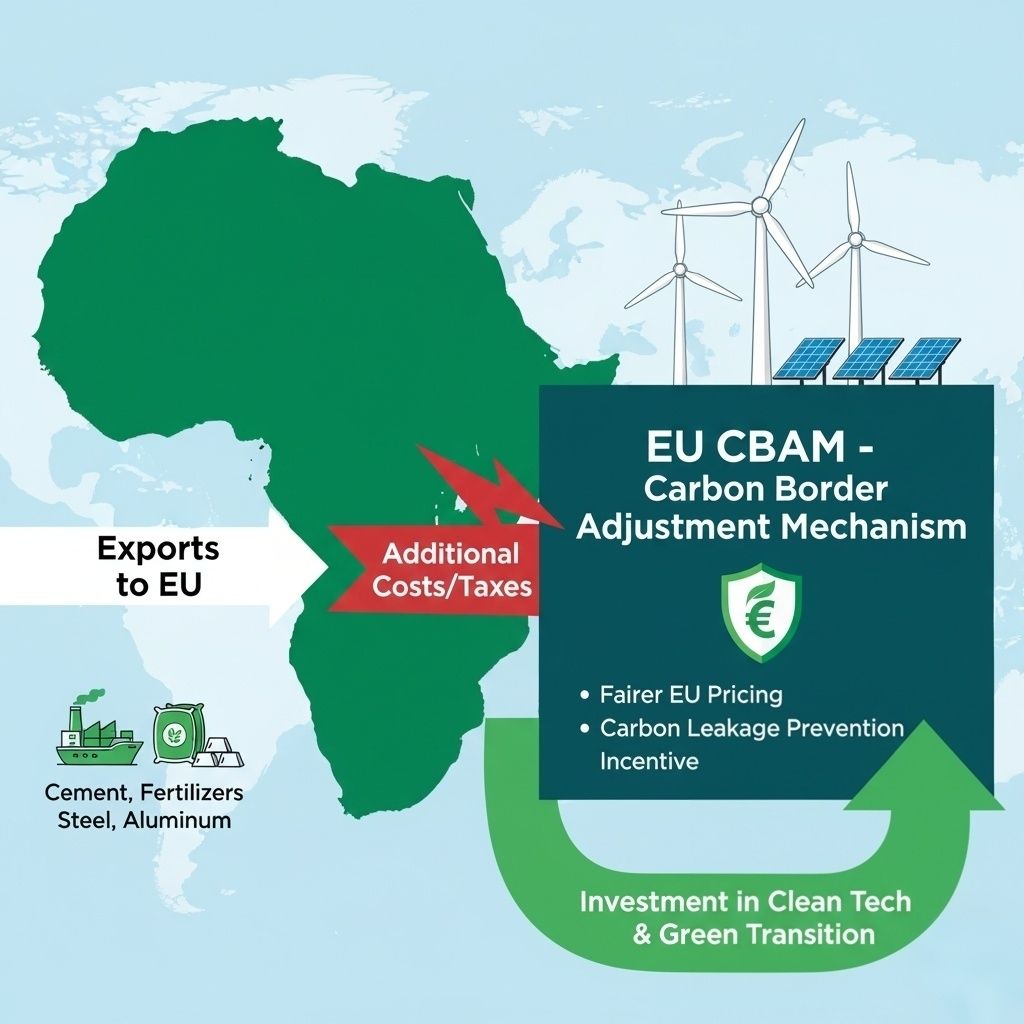

- CBAM / Carbon Border Adjustment Mechanism - update and trajectory.

CBAM / Carbon Border Adjustment Mechanism - update and trajectory.

Europe-Africa Initiative

October 25, 2025

Recent developments

CBAM will commence its application (to selected sectors) in 2026 and may be extended in time. The EU (and its stakeholders) ponder on the scope to expand the product coverage (beyond the current industrial goods), the effectiveness of credits or rebates to the exporting countries with the carbon tax or mitigation measures, and the calibration of the CBAM to prevent legal as well as fairness/ WTO lapses. Analyses published by the IMF The EU's CBAM: Implications for Member States and Trading Partners in have shown that CBAM might introduce further demand burden of carbon cost on imports and alter trade patterns.

African think tanks and climate policy groups have cautioned that the CBAM can discriminately affect economies of developing countries by increasing administrative expenses, lowering competitiveness, and an effective carbon tariff with inadequate consideration of climate justice advocacies.

According to the IMF, the aim of CBAM is to eliminate carbon leakage, the implications and measurement of the carbon value in the real world will be determined by the method of computing embedded carbon, the amount of exemptions and compensation permissible, and the treatment of the rebates and credits.

Implications to Nigeria and the EU

For Nigeria:

● Export competitiveness risk: The export competitiveness of Nigeria is at risk because the exports, especially in the cement, fertilizer, steel and aluminum sectors are worth billions of dollars and this risk may have a huge impact once the carbon costs are implemented in the EU market. These supplementary costs can either lower the profit margins or even drive the Nigerian exporters out of business unless they make the effort of decarbonizing the production processes.

● Carbon accounting and investment in mitigation: To be viable under CBAM, the Nigerian producers will require carbon accounting, emissions monitoring, cleaner production, energy efficiency, and even carbon offsetting.

● Administrative and verification cost: Exporters will be subjected to presenting data on emissions, audit, documentation and potential third-party verification which could be expensive and may be complicated, particularly at the technical level, especially to smaller firms.

● Climate-green investment opportunity: The pressure might facilitate green investment (renewables, energy transition) funded either domestically or through climate and development aid.

For the EU:

● Use climate diplomacy leverage: CBAM reflects the EU aspiration to make trade climate-consistent and can compel partner nations to decarbonize with the global climate objectives.

● Law and business risks: EU should make sure that CBAM does not conflict with WTO regulations and does not face the accusation of protecting the domestic market; the trading partners may argue or even retaliate.

● Complexity in operations and administration: The EU (member states) will require an instrument to check, audit, enforce and inspect carbon content in imports of goods, which is a resource-consuming procedure.

● Threat of backlash and equity issues: EU will receive criticism (particularly by developing nations) that CBAM imposes unjustifiable burdens, breaches the concept of common but differentiated responsibilities (CBDR), or other attempts to block industrialization in poorer countries.

Suggested future actions

For Nigeria:

● Sectoral carbon preparedness scan: Determine what export sectors will be covered by CBAM and the preparedness of those industries in relation to emissions data, process emissions, energy consumption, and cost arrangements.

● Pilot emissions reporting systems, pilot audit systems: Co-operate with willing exporters (particularly in steel, cement, fertilizer) to pilot carbon accounting, external check, and internal control of emissions.

● Clean tech incentive schemes: Develop tax breaks, subsidies or incentives to firms that adopt clean energy, energy efficiency upgrades or capture carbon solution.

● Regional / African coordination: liaise with ECOWAS/AFRICA trade groups to come up with a joint African negotiating position or concerted reactions to CBAM (e.g. common carbon reporting rules) to prevent fragmented actions.

For the EU:

● Differentiated treatment of developing exporters: Introduce transitional relief, low income exporters or developing sector allowances or exemptions in order to mitigate too much disruption.

● Helpful mechanisms: Fund and technical support to the exporting nations (such as Nigeria) to enhance abilities in emissions reporting, cleaner production, capacity building.

● Clear methodology and stakeholder consultations: make sure that calculations of carbon content, rules on offsetting, and verification systems are open and consistent and discuss them with the exporting nations.

● Laws and regulations: Laws and regulations: Formulate CBAM regulations that would meet the WTO standards and would have a clear appeal or review process.

Reply